Safeguarding Pension Assets in Turbulent Markets Through Affordable Housing

By: Deborah LaFranchi, American South Capital Partners

For decades, institutional investors assumed that affordable housing could not generate alpha. That perception is now being overturned as economic and demographic forces reveal affordable housing to be one of the most resilient real estate strategies available — particularly valuable for pension funds seeking stability in volatile markets. These forces are “turning a social challenge into a compelling financial opportunity.”

The foundation of this resilience lies in a structural shortage of affordable units. The United States faces an estimated deficit of seven million affordable homes, a gap that continues to widen. This shortage has pushed more than half of all renter households into being cost-burdened, spending over 30% of their income on housing. With so few alternatives and limited new construction, demand for affordable units remains exceptionally steady even when the broader economy contracts. Research shows that newly constructed units lease up rapidly, often with waitlists forming before construction is complete, a dynamic that provides unusually reliable occupancy and income streams.

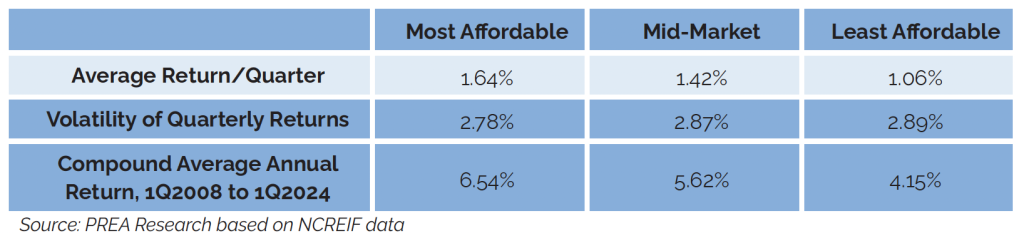

This stability is especially important for pension funds, which must match long-term liabilities with dependable cash flows. Affordable housing’s performance is further strengthened by its low correlation to macroeconomic cycles. Studies from NBER, Nuveen, NCREIF, and others show that affordable housing consistently exhibits lower vacancy rates and less sensitivity to economic downturns than market-rate multifamily housing. A 2024 PREA study found that over a 16-year period, the average annual return of the most affordable properties serving households at or below 80% of area median income outperformed higher income properties by 239 basis points, largely due to lower tenant turnover. In an environment where public markets can swing sharply, this kind of predictability becomes a powerful safeguard for pension portfolios.

The supply/demand imbalance is poised to intensify. Rising construction costs and higher interest rates have made new development far more expensive. Construction lending rates have climbed from around 4.5–5.5% in 2018 to as high as 7.5–9%1, while materials such as steel and concrete are “up over 40%”2. Developers have responded by shifting toward higher income projects where elevated rents can offset these costs. Between 2022 and 2025, more than two million multifamily units were built3,4 of which 13% were affordable. It is estimated that between 2026 to 2029, total production is projected to fall by a quarter, with only 38,000 affordable units expected in 20295. This steep decline in supply reinforces the defensive nature of affordable housing: even as economic conditions fluctuate, the scarcity of units ensures persistent demand and stable revenue.

Historically, affordable housing relied heavily on the federal Low Income Housing Tax Credit program. But inflation and rising interest rates have eroded the effectiveness of these subsidies, which now cover a shrinking share of project costs. Developers often must assemble 6–11 sources of government subsidy, stretching timelines to 3–5 years for a single project. This complexity has pushed many developers to seek private capital, which offers speed, flexibility, and the ability to capitalize on local and state incentives. In Texas, for example, qualifying projects can receive a 100% property tax exemption, boosting net operating income by 20–25%. These incentives, combined with mixed income models that blend affordable, workforce, and market rate units, create strong economics that can support attractive returns.

For pension funds, the appeal lies in the combination of competitive returns and downside protection. Equity returns for well-structured affordable housing projects often fall in the mid-teens to low twenties, supported by high occupancy, reduced turnover, and favorable local incentives. Unlike many real estate sectors, demand for affordable housing tends to increase during economic uncertainty, as families “tighten budgets, seeking stability and lower rents.” This countercyclical behavior makes affordable housing a rare asset class that can strengthen a portfolio precisely when other investments falter.

The investment landscape has also matured significantly. Twenty years ago, few institutional grade managers operated in this space. Today, a growing cohort of specialized firms has more than a decade of track record, giving pension funds the data and confidence needed to underwrite the strategy. As Peter Braffman of GCM Grosvenor observes, affordable housing is now viewed “very differently — and far more positively” than before the Global Financial Crisis.

For pension funds navigating turbulent markets, affordable housing offers a compelling blend of resilience, diversification, and long-term value. Its structural demand, limited supply, and low correlation to economic cycles create a defensive real asset strategy capable of delivering stable income and protecting capital. At a time when many portfolios are overexposed to high income housing or public market volatility, affordable housing stands out as an investment opportunity hiding in plain sight — one that aligns financial prudence with meaningful social impact.

Deborah La Franchi is the founder and CEO of SDS Capital Group. SDS is a recognized national leader in impact investing with $1.7 billion of active assets under management. Through a family of innovative funds, SDS engages the private sector in the meaningful investment in underserved communities with the mission of promoting economic development and creating affordable supportive housing for marginalized families throughout the United States. As head of the investment committee on each of the firm’s six separate funds, Debbie leads the investment strategy, fundraising, and oversight of senior managers.

Debbie earned a BA in Political Science and History from UCLA, an MBA from UCLA, and an MPP from Georgetown University. She also holds a Series 65 license.

Endnotes:

1. Federal Reserve Bank of New York, “Secured Overnight Financing Rate Data,” Markets & Policy Implementation: Reference Rates, 2025

2. Federal Reserve Bank of St. Louis., Producer Price Index by Commodity: Special Indexes: Construction Materials

3. Federal Reserve Bank of St. Louis., Producer Price Index by Commodity: Special Indexes: Construction Materials

4. Yardi Matrix, “U.S. multifamily supply up and rents down,” Yardi Matrix, Oct. 30, 2024.

5. Yardi Matrix, “Multifamily Forecast Sees Higher Completions Through 2027,” CRE Daily, Aug. 8, 2025.